The Daily Trades 27/07/2026

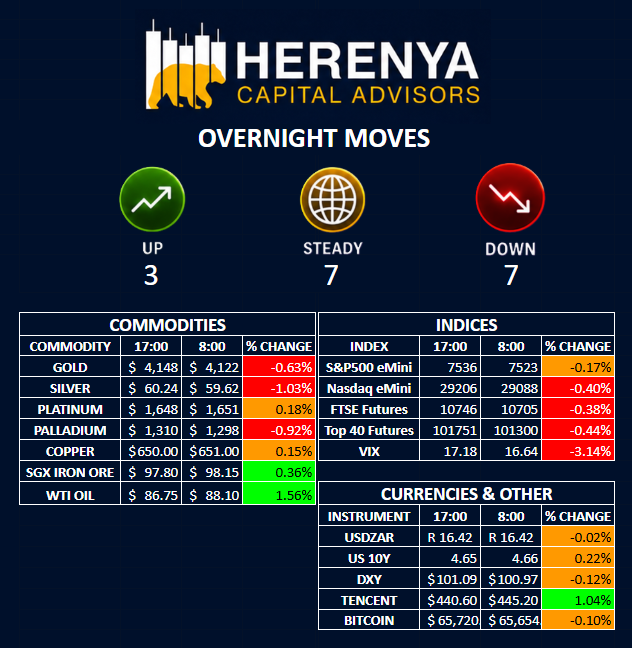

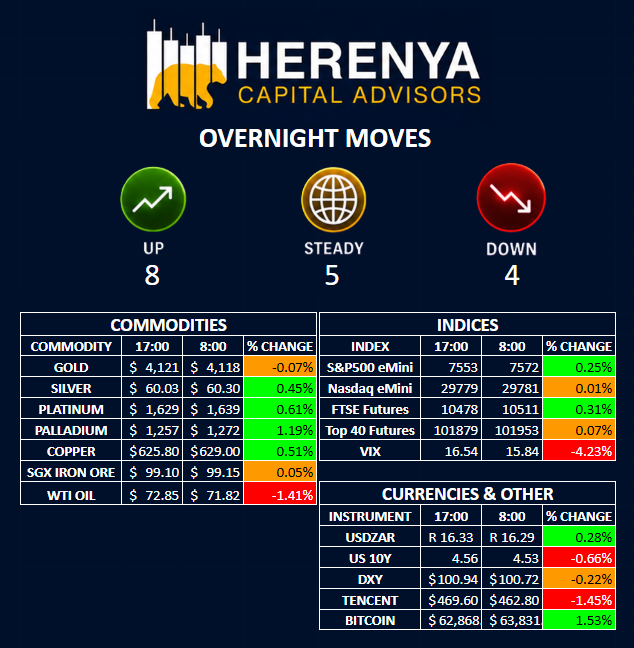

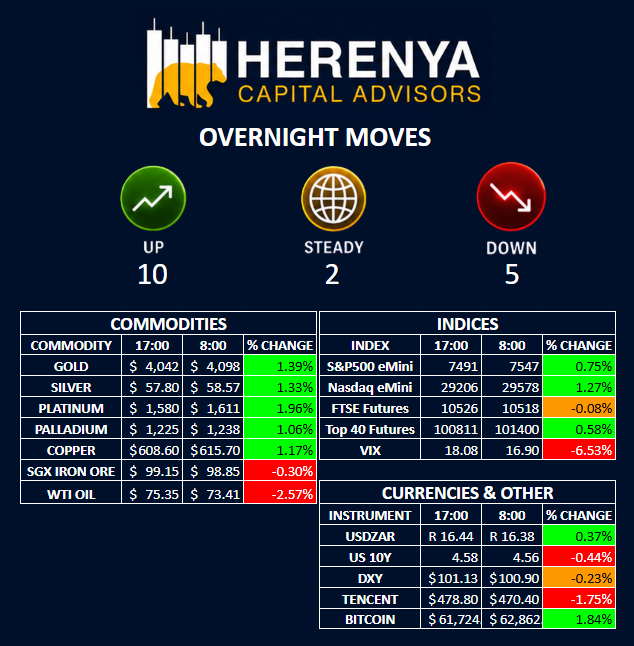

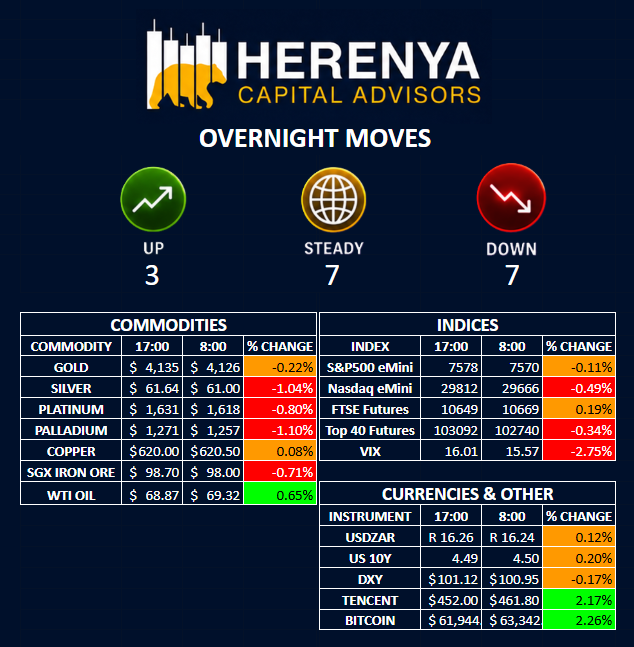

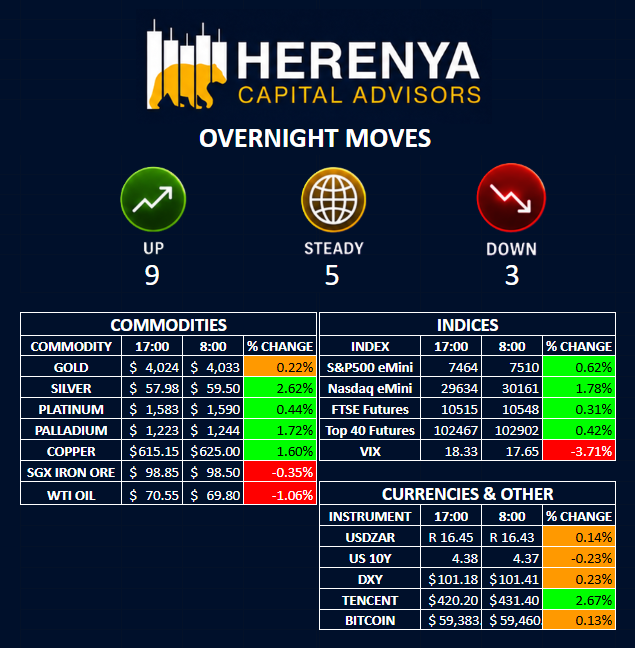

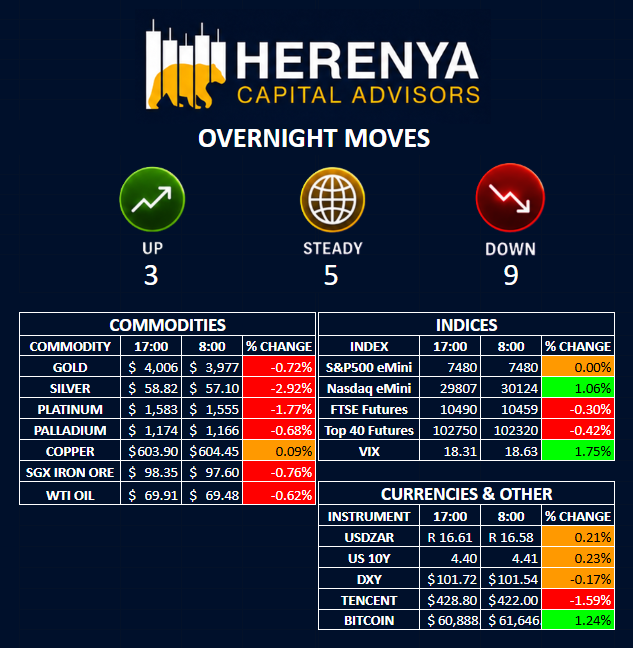

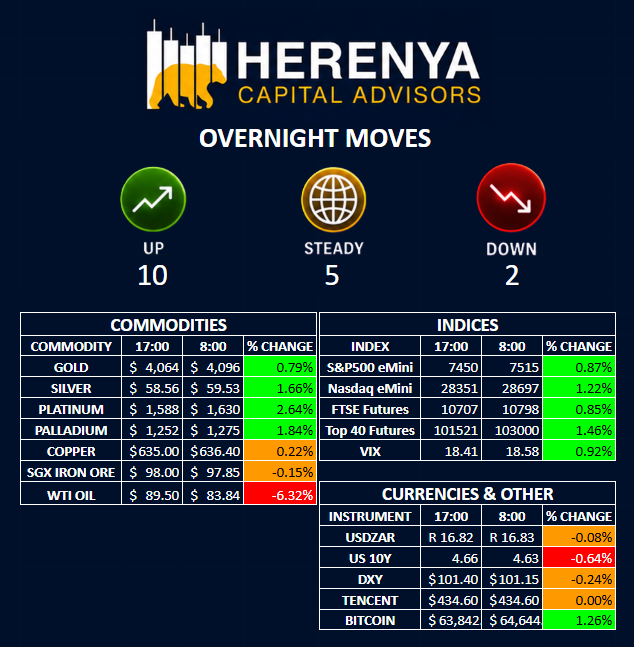

Market Overview The following is a partial recap of the market analysis shared during today’s morning Discord call. We open the day to a market rally in commodities and equities, following the cancellation of planned strikes over the weekend. Oil is the main loser today as it dropped by 6%, while gold and PGMs (Platinum […]

The Daily Trades 27/07/2026 Read More